- India is categorized as a ‘leader’ or ‘strong’ in respect of 25 (21 in the previous exercise) out of 40 indicators and

- Categorized as ‘weak’ in respect of 8 (12 in the previous exercise) indicators.

- Significant progress and moved to a leadership position in large value payment systems and fast payment systems, which contributed to rapid growth in digital payments.

- The exercise highlights that there is scope for improvement in acceptance infrastructure i.e. ATMs and PoS terminals.

Tag: Infographic

Customer Centricity is at the Core of RBI

The Numbers & The Story?

———————————-

- Customer Centricity is at the Core of RBI

- Nation-wide Intentive Awareness Program (NIAP) was launched by RBI on Nov 22

- Focus to create financial awareness among the Tier III to VI population (Unbanked & Underbanked)

- Campaign Outreach

- Online – 25 Crore people

- Physically – 3 Crore people

- 16000 – differently abled

- 22000 – Senior Citizens

- Impact

- Due to awareness levels, the surge in complaints

- Customer care calls up

- Complaints via the Online portal have increased

The 2022 Crypto Crime Report

Overall, going by the amount of cryptocurrency sent from illicit addresses to addresses hosted by services, cybercriminals laundered $8.6 billion worth of cryptocurrency in 2021.

That represents a 30% increase in money laundering activity over 2020, though such an increase is unsurprising given the significant growth of both legitimate and illicit cryptocurrency activity in 2021

Overall, cybercriminals have laundered over $33 billion worth of cryptocurrency since 2017.

Factoring Services

What does it tell us?

RBI issues regulations under the amended Factoring Regulation Act, 2011

- The government of India has recently amended the Factoring Regulation Act, 2011 which widens the scope of companies that can undertake factoring business.

- Further, the Act empowers the Reserve Bank of India to make regulations prescribing the manner of granting a certificate of registration and for prescribing the manner of filing of assignment of receivables transactions by TReDS on behalf of the Factors.

Banks’ Lending to NBFCs in India

What does it tell us?

Banks’ Lending to NBFCs in India

- Amongst scheduled commercial banks, public sector banks (PSBs) remained dominant lenders to NBFCs, although private sector banks expanded lending to NBFCs in 2020-21

- Overall bank exposure to NBFCs grew as their investment in NBFCs’ debentures increased on the back of COVID-19-related schemes.

Assets quality of NBFCs in India

What does it tell us?

Assets quality of NBFCs in India

- Both Gross NPA and Net NPA ratios declined post-March 2020. The higher provision coverage ratio (PCR) during the period is reflective of adequate buffers to deal with likely headwinds.

- In 2021-22 (up to September), the asset quality of the sector deteriorated to some extent. GNPA ratio increased from 6.0 percent to 6.8 percent and the NNPA ratio increased from 2.7 percent to 3.0 percent.

Loans to MSMEs by NBFCs in India

What does it tell us?

Loans to MSMEs by NBFCs in India

- The MSME sector was among the most pandemic-afflicted sectors

- NBFCs’ credit to MSMEs grew at 17.8 percent during 2020-21. ICCs, together with NBFCs-MFI, are the main purveyors of MSME credit

- Eleven percent of the NBFCs-MFI’s loan book comprises micro and small loans

Distribution of Retail Loans of NBFCs in India

What does it tell us?

Distribution of Retail Loans of NBFCs in India.

- Vehicle loans credit, the largest segment in retail loans, witnessed a reduction in share during 2020-21 owing to a disruption of activity.

- Vehicle financing is a niche area for NBFCs in which they still account for a predominant share.

- While the share of lending against gold doubled

- Indicators of sales of Commercial, Passenger, and Tractor sale is also provided.

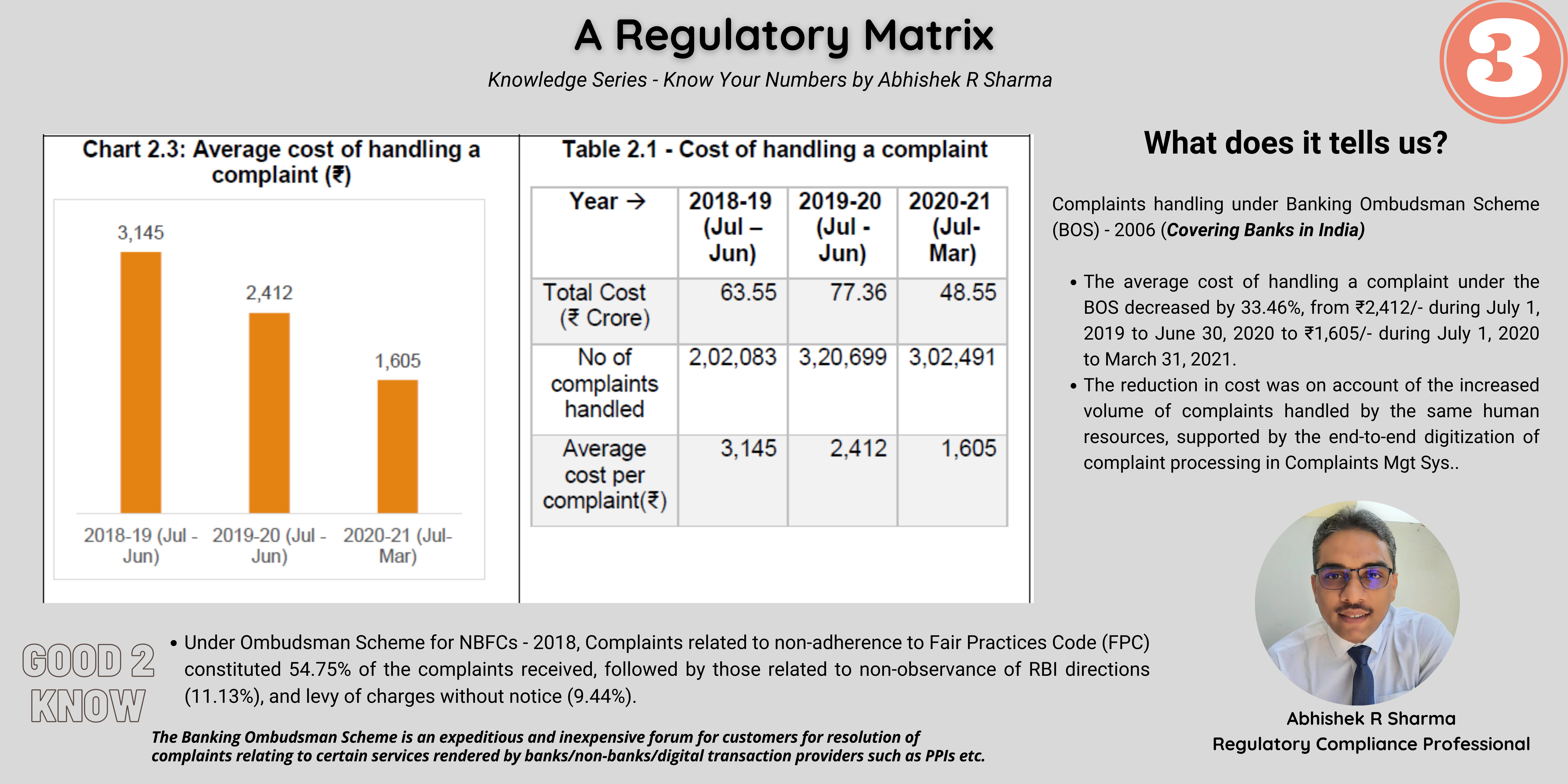

Cost of Handling Complaints – RBI

What does it tell us?

Complaints handling under Banking Ombudsman Scheme (BOS) – 2006 (Covering Banks in India)

- The average cost of handling a complaint under the BOS decreased by 33.46%, from ₹2,412/- during July 1, 2019, to June 30, 2020, to ₹1,605/- during July 1, 2020, to March 31, 2021.

- The reduction in cost was on account of the increased volume of complaints handled by the same human resources, supported by the end-to-end digitization of complaint processing in Complaints Mgt Sys.

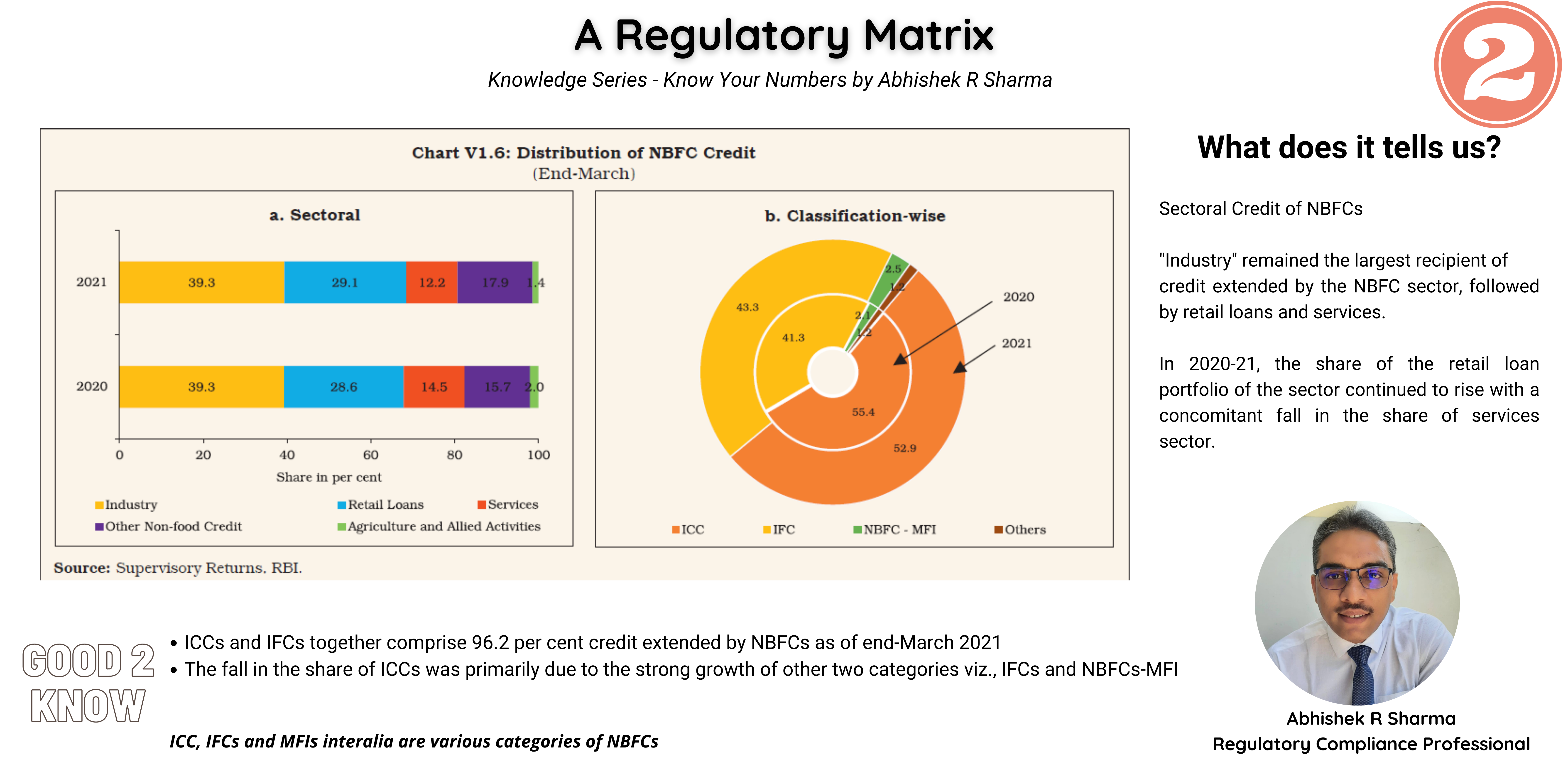

Distribution of NBFC Credit

What does it tell us?

Sectoral Credit of NBFCs

“Industry” remained the largest recipient of

credit extended by the NBFC sector, followed by retail loans and services.

In 2020-21, the share of the retail loan portfolio of the sector continued to rise with a concomitant fall in the share of the services sector.